06 Nov Institutional Investing (Asset Owner)

A long ‘work-in-progress’ post on Institutional Investing from the perspective of an Asset Owner.Main Investment Considerations

Investment Philosophy – Asset Owner

Asset owners’ investment philosophy can be broadly categorized into Yale model, Norway model and Canada model.

Yale Model (also known as Swensen Model or Endowment Model): This refers to an investment program diversified into alternative asset classes, combining reliance on the equity premium, illiquidity premium and hedge fund alpha. Endowments tend to employ this model, taking relatively higher risks with a longer term investing outlook.

Norway Model: This refers to an investment program employing the traditional 60-40 type portfolio with large internal staff managing in house. Returns would be derived mainly from traditional asset classes’ Beta. As the name implies, this is the investment philosophy of Norway’s sovereign wealth fund. Small asset owners who require higher liquidity and maintain a small investment team would find the Norway Model suitable as well. Similarly, returns would be derived from market Beta but the allocations can be outsourced to external fund managers.

Canada Model: This refers to an investment program focused on private markets and illiquid assets. The ability to hold investments for the long term is critical as liquidity is compromised to reap illiquidity premium. In addition more due diligence capabilities are required for private market investments.

Importance Of Diversification

Diversification helps to lower overall risk of a portfolio when different asset classes or strategies with low or negative correlation are put together.

The difficulty in achieving effective diversification lies in identifying asset classes that exhibit low or negative correlation. Correlation can change drastically during crisis periods when asset classes which are normally uncorrelated become highly correlated. This renders the perceived diversification benefits useless.

Importance Of Long-Term Investing

It is important to align the risk premium we are trying to extract from markets or the strategy we are employing to the correct time horizon. Most risk premiums need time to ride out shorter term fluctuations hence it is very important to stick to the investment plan and think long term. Typically 5-7 years are required for a full market cycle.

Thinking long term also helps to avoid behavioural mistakes of greed and fear which often causes investors to make investing entries and exits at very wrong times.

Strategic Asset Allocation

Strategic asset allocation is traditionally viewed as the most important decision in the investment process as majority of a portfolio’s returns are driven by it.

The long term Strategic Asset Allocation can be used as a reference portfolio from which we try to enhance risk-adjusted performance.

Traditional Asset Allocation Frameworks

Mean variance optimization is a traditional asset allocation framework frequently used. Mean variance optimization results can be unstable when the covariance matrix is ill conditioned. This is caused by using similar assets. Covariance matrix is the combination of correlation and volatility. Mean variance optimization results are highly sensitive to inputs. Small input differences can lead to large output differences. As a result, mean variance optimization produces extreme weights that fluctuates substantially over time and performs poorly out of sample. Mean variance optimization models did not perform well in real life.

CAPM model says that the beta coefficient tells us the sensitivity of an asset’s excess return to variations in the market’s excess returns. In real life, returns of high beta portfolios were too low and returns from low beta portfolios were too high. CAPM was expanded from a single factor model to 3 factors model including value and size. Carhart (1997) added a fourth factor: cross sectional momentum. The greatest problem with CAPM is that market prices do not follow a normal distribution. Prices have unstable variance and fatter tails with extreme events happening with higher frequency.

CAPM assumes that investors agree on returns, risks, and correlation characteristics of all assets and invest accordingly. This is rarely true.

Risk Parity Approach

Following the Global Financial Crisis in 2009, risk parity approach to asset allocation has risen in popularity. Risk parity approach aims to equalize stock and bond volatility. Hence risk parity portfolios tend to have higher bond allocations. Leverage is typically employed on bonds to enhance expected returns up to acceptable levels.New Approaches to Asset Allocation

AQR has articulated a new approach to asset allocation:

Think of return sources of a portfolio as a pyramid with three layers, starting from the base, with the highest capacity and lowest cost structures, and moving up to the top, with the lowest capacity and highest costs.

Market risk premia form the base and are the rewards for stable long only holdings in major asset classes. These include equity risk premium, term premium, credit premium and commodity premium.

The middle layer consist of alternative premiums such as value premium, premium to basic convertible or merger arbitrage, premium to carry strategies and the extra expected return from accepting illiquidity.

True alpha is elusive and scarce and is the top of the pyramid.

At the base layer, risk allocations should be used through a risk parity allocation approach in which several market risk premia are balanced. One example of risk parity portfolio is a third of the risk budget in global equity for growth, a third in global government bonds for deflation protection and a third in real assets such as commodity futures and inflation linked bonds for inflation protection.

Apart from AQR’s description, the table below shows the various asset allocation approaches:

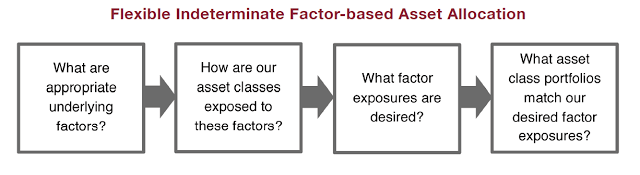

Harvard Endowment recently showcased their new asset allocation process as below:

Portfolio Rebalancing

After the Strategic Asset Allocation is implemented, changes in price affect market value of asset classes. Portfolio rebalancing brings the weights back to policy weights. Portfolio rebalancing is also sometimes done during manager re-allocation or used to express short term tactical views.

The 3 main considerations in thinking about whether rebalancing is required are namely risk, return and cost implications.

1) Risk: A portfolio becomes less diversified over time as winners have bigger weights and losers have smaller weights. Rebalanced portfolios are likely to retain their portfolio level risk characteristics better. 2) Return: Passive rebalancing should be viewed as an active contrarian strategy. Rebalancing to constant weight involves selling winners and buying losers. This tends to be profitable during periods when investments have mean-reverting performance. 3) Cost: Rebalancing incurs transaction costs.

If rebalancing is viewed to be necessary, then we need to think about:

1) When to rebalance? (How often? Fixed schedule or trigger-based system?) 2) How much to rebalance? (Fully back to the benchmark, or only partially?)

There are three main determinants of which method may be preferred for a given investor, relating to risk preferences, costs and return expectations.

Determinant 1: Tolerance of short-term variations in portfolio risk characteristics. However we note that most rebalancing processes will maintain long term risk characteristics almost equally well. Determinant 2: Expected costs including transaction costs, operational costs and tax implications. Determinant 3: Expectations of trending or mean reverting investment performance. If investment returns exhibit trends or mean reversion, the rebalancing frequency can affect expected portfolio returns. Rebalancing at or within the frequency of any mean-reversion patterns will tend to earn positive returns, while rebalancing at or within the frequency of any momentum effects will be fighting against these and therefore tend to suffer negative returns.

There is evidence that many investments exhibit 3- to 12-month momentum, which may be exploited by less frequent rebalancing (annual or lower frequency). This can allow winning and losing trends to “play out” and compound between rebalances.

AQR documented hypothetical performance of different rebalancing methods including calendar based rebalance and trigger based rebalance.

The result shows biennial and annual rebalancing outperforms. The frequently rebalanced portfolio suffers a drag from short-term momentum, but earns a bonus from longer term mean-reversion. Annually or biennially rebalanced portfolios, however, get the best of both worlds in this sample: they behave like buy and- hold portfolios at shorter horizons (harnessing momentum), but like rebalanced portfolios at longer horizons (harnessing reversals). Trigger-based processes appear not to enjoy the same advantage. For example, the +/–20% threshold triggers roughly one full rebalance per year on average, and achieves tighter allocation ranges than a fixed annual process, for similar turnover. However, it underperforms the latter, probably because it tends to trigger rebalances during trend events. Details shown in table below.

Active vs Passive

The decision to employ active or passive management is determined by the characteristics of the asset class.

For example, there has been a lot of research regarding efficiency of markets and the table below shows the academic research for Asia Pacific Equities. We can see that in general developed markets are more efficient and hence there is more scope for engaging passive managers. In developing markets active management may add alpha provided the fee difference is not too much.

External Multi-asset investing

Institutional investors’ decision making process is often slow and cumbersome due to the bureaucracy and internal control processes which requires multiple levels of approvals for most decisions.

To navigate a volatile market environment, it may be beneficial to engage external managers to run Absolute Return Multi-asset. The first benefit is the nimbleness of the external manager. They can invest in more asset classes and implement their investment views in a faster manner. The second benefit is that the external manager may produce return streams which are less correlated with the investment program’s returns. This is due to the difference in strategy between the asset owner’s investment program and the external manager’s multi-asset investments.

For example, if the external manager can invest in commodities and alternatives when the investment programme cannot, the return stream might be less correlated.

Currency hedging

Source: BNP Paribas

Smart Beta

Smart Beta is a general term referring to non market cap weighted indices. Beta is neither smart nor dumb, just like standard deviation or correlation is neither smart or dumb. Hence some firms have started using the term Strategic Beta instead of Smart Beta.

The increased interest in Smart Beta can be largely explained by a growing awareness of the alternatives and potential benefits to the market cap index investment process.

Smart Beta has enabled investors to get access to different kinds of risk premia at reduced fees.

Asset owners who have taken money away from passive managers as putting it into smart beta strategies with tracking errors in the 0.5-1 per cent range. These are highly diversified factor strategies with a large number of holdings and very low stock specific risk. By contrast, where investors are moving money away from active managers, they are happy to go with tracking errors of 2-3 per cent.

Asset owners have used it to get exposure to particular risk factors that were attractive at a point in the investment cycle or to manage exposure to a particular asset class or sector where the fund might want exposure or avoid. It might also have been done for cost reasons and where the asset owner had lost faith in active management, but not in a particular factor.

One other way of using Smart Beta is to combine multiple risk factors together in a Multi-Beta portfolio. This diversifies the portfolio in terms of risk factors and avoids timing the factors as different factors perform differently in different market environments.

Some common risk factors are:

Source: ScientificBeta

Investment Implementation

Manager research and selection

Past performance does not guarantee future performance but it seems that institutional investors are still falling prey to performance chasing. The diagram below shows that investors fired their underperforming manager and invested with the outperforming manager but after changing managers, the incoming manager underperforms the outgoing manager.

The lesson is that “past performance does not guarantee future performance” is factual. Different strategies perform well during different market environments. The focus must be on understanding the strategy and discerning whether the underperformance is due to a cyclical nature in an disadvantageous market environment or due to a permanent failing of the fund manager.

The diagram below illustrates the fund manager lifecycle. Funds entering the growth phase has demonstrated some degree of success with sufficient capacity to take on more assets without compromising performance.

List Of Questions For Fund Manager Meeting

Introductory questions • What are the asset classes that your AM firm excel in? • Are they active/passive? • Fund size? How many % of investors are institutional? How many % are from SG Institutions? • Any Singapore office? If yes, what’s the breakdown of manpower (e.g. FM, RMs, Ops) • Economic outlook? Product • What is the benchmark? • Any SGD share class? • Hedging of currency exposure provided? • Risk and return targets? • Investment process to attain the risk and return targets? – Use of derivatives? Leverage? – What is the average holding period for the securities? – How does the team derive at each buy/sell decision? – How has the portfolio perform in this recent economic environment? And how might your portfolio perform in the near term given the economic outlook? • Track record vs peers and benchmark (both returns and risk) • Fund rated by Consultant? If so, which consultants? Fund Management Team • Size, location and experience of Investment Team • What makes your asset management firm stand out from your competitors in this asset class?Request For Proposal Questionnaire For Fund Manager

Section 1 : Background of firm

• Describe the firm’s current lines of business. • Describe any changes in the overall business philosophy, strategy or business plans for the firm over the past 5 years. • If applicable, describe significant legal issues facing the firm. Indicate whether the firm been subject to any judgements, indictments, or settlements with or without admission of guilt in the past year. If so, please provide a full explanation. • Has your firm changed auditors in the past 5 years? If so, please provide the reasons for the change. • Describe the Client base (i.e. govt and non-govt clients) and total assets under management over the last 5 years (overall and xxx mandates). • Indicate whether your firm is involved in any talks with other organizations on mergers and acquisitions of your fund management business currently. Indicate whether there are any merger and acquisition plans involving your firm in the near future. Please elaborate if any of the answers is ‘yes’. • Please provide a summary on the state of your firm’s financial health during the past two years highlighting any negative events or developments that may have an adverse impact on your operations. • Please summarize your disaster recovery plans. Indicate whether you have secured an alternate site for maintaining critical functions and the expected time delay until critical functions are up and running at the alternate site. • Please state the physical location of the relevant personnel involved with Investment, Trading, Administration and Operations functions for the fund.

Section 2 : Investment Process & Risk Controls

• State your firm’s investment philosophy, and in particular to xxx. • Provide details on your investment process and research capabilities. Include a description of how individual research ideas make it / don’t make it into the portfolio. • What is your sell process? Please list 3 largest percentage losers currently in the portfolio and explain the investment thesis for each. • Do you set price targets for all purchases and if yes do you ever hold a security beyond the initial price target? Explain. • What is your investment edge? What differentiates you from your competitors? Include a list of firms that you consider to be your biggest competitors. • In what environments will this strategy perform the best and worst? • Provide details of your risk management process. • Explain how your firm ensures that clients’ portfolios complies with clients’ guidelines at all times. Also, please describe the controls in place to prevent unauthorized trading in the account. • List your firm policies relating to client confidentiality, trading policy for employees, best execution policy, trade allocation process on block/aggregating trades, allocation for partially filled trades between different clients (e.g. pro-rata), allocation for primary issues and partially filled primary issues between different clients and managing conflicts of risks • Describe your firm’s use of soft dollars, or commission recapture/rebate practices. Please provide a copy of your firm’s policy regarding Soft Dollar Arrangements.

Section 3 : Characteristics of Proposed Solution

• Indicate whether the Proposed Solution is a segregated account, a new fund to be established or an existing fund(s) that are offered by your firm. • For commingled fund structure, who is the custodian bank, how often do you perform reconciliation with custodian bank and what pricing source is used? When you find pricing differences what is your procedure for reconciliation? • Explain the investment strategy and style of the Proposed Solution. • State the most appropriate benchmark. If the benchmark is not the xxx Index in Singapore Dollars term, please specify the strengths of the Alternative Benchmark proposed, and why it should be adopted. • List the investment guidelines of the Proposed Solution and highlight any proposed changes or additions to the Investment Guidelines in Appendix A (if applicable). • Elaborate on the liquidity of the Proposed Solution. If an index fund is proposed, please indicate the frequency at which subscriptions and redemptions can be executed. If an exchange traded fund is proposed, please indicate a typical bid-ask spread and the daily exchange turnover of the exchange traded fund. • Provide ex-ante estimates of the Proposed Solution’s return and standard deviation, and explain how these ex-ante estimates are derived. • Provide current portfolio characteristics such as (Price to Earnings ratio, Price to Sales Ratio, Earnings Growth, Sector Weights, Industry Weights, Percent of fund in top 10 holdings etc) (Effective Duration, Credit Rating Allocations, Sector Allocations etc) • Provide the 1 day, 10 day, 30 day Value at Risk for current portfolio. • Describe how the Proposed Solution is expected to perform in times of market stress, for example provide figures on how the Proposed Solution fared in the global financial crisis in 2008/2009. • What is the fund’s capacity? At what point would you close the fund to new clients? At what point would you close the fund to new assets from existing clients?

Section 4 : Track Record

• Provide the performance track record of the Proposed Solution against the xxx Index in Singapore Dollar terms, over last 1, 2, 3 and 5 years ended xxx and since inception in SGD : – Both annualised and monthly returns gross of fees – Both annualised and monthly returns net of fees – Both annualised and monthly excess returns gross of fees – Both annualised and monthly excess returns net of fees – Standard deviation – Kurtosis – Skewness – Tracking error – Information Ratio – Portfolio turnover – Maximum drawdown – Ratio of expenses to NAV, including and excluding management and performance fees • Monthly returns in Singapore Dollars of above portfolio and its benchmark over last 5 years ended xxx and since inception (please provide soft copy of return data). • Include full performance disclosure and composite information, if applicable. These include: – number of accounts included in composite and assets of those accounts, – number of accounts managed in similar style but not included in composite and assets of those accounts, reasons why those accounts are not included -number of accounts added to or subtracted from the composite in each year. • Provide annual performance attribution for the past 5 years.

Section 5 : Investment Team

• List the experience of key decision makers. • Describe the structure of the investment management team. Who actually makes buy and sell decisions? Who is the lead portfolio manager and who is portfolio manager backup? • Indicate whether there are any major changes in the key personnel over the last 5 years. If yes, please provide details. • Regarding the portfolio manager or team that would manage our fund, please describe the number of accounts and total assets for which the manager or team has responsibility. • Describe compensation structure of the firm’s portfolio managers and research analysts including incentives, bonuses, performance based compensation and equity ownership.

Section 6 : Total Expense Ratio and/or Fund Management Fee

• Please indicate the total expense ratio and/or fund management fee. If applicable, please indicate the breakdown of the Total Expense Ratio showing the charges for Fund Management Fee. Note that if the proposal is accepted, the accepted total expense ratio and/or fund management fee shall not be varied during the term of the Contract.

Section 7 : Others

• Provide sample of portfolio/market/economic reports sent to clients • Indicate the time lead required to invest into the Proposed Solution. • Indicate the estimated costs of investing into the Proposed Solution e.g. brokerage fees, taxes etc. • If applicable, indicate the training to be provided to our staff, e.g. IT system that provides account information of the Portfolio. • Provide at least 2 local client investors (preferably one of which is a government–related client) from whom we may contact for a confidential reference.

Preparing For On Site Visit

Interview with Investment Professionals

• We need to spend time with key investment personnel and also all secondary and supporting investment personnel. This includes analysts, traders and any other person who might have a role in the management of the product. It is best to spend time alone with each if possible. • Preferable to conduct discussions at their desks • Always ask to see actual examples of individual’s work • Ask to sit in for investment meetings or morning meetings.

General questions for Investment Professionals:

• Who is in charge of the day to day management of the portfolio? • How do the different members of the investment team work together? • What are each of the investment professional’s responsibilities? • What areas of specialization (if any) do each of the investment professionals’ concentrate on? • Who is responsible for trading the portfolio? • Who is the lead portfolio manager’s backup? (if any) • What is the process the firm uses to select buy candidates and what criteria are used to identify sell candidates? • What are some specific examples of securities that you have purchased and sold? • How is the portfolio constructed? Are there constraints on position size, sectors, industries, or fundamental characteristics? • Who is in charge of the portfolio’s asset allocation? What systems do they use to assure that portfolios are allocated properly? • Who is in charge of conducting portfolio risk analysis? • What systems and other resources are used by the investment staff and how are they each applied to the product under review? • Are any of the investment staff working on any other products? • How often does the investment staff meet to discuss the portfolio? • Have any investment professional’s roles changed within the firm or with regard to the product in question? • What is the firm’s sell discipline? • What level of research is conducted on each securities in the portfolio and under review for possible inclusion in the portfolio? • What constraints have been put on the portfolio and how are they enforced?

Individual questions for Investment Professionals:

• What is your investment experience? • Have you changed your style of investing during your career? Has your style of investing evolved over your career? • What are the best and worst investment decisions you have made for the product under review? • How do you personally interact with your fellow investment staff? • Can you go through in detail some of the stocks that you have researched that are in the portfolio? • Can you take me through your personal investment process by picking a security you are currently researching and bring me up to speed on your progress? • Can you give me a demonstration of your firm’s technical research and portfolio management capabilities? • Which brokerage firms conduct the bulk of your trades and what is your average commission? • What are your strengths and weaknesses? • Can you provide personal references from your previous employment?

Marketing personnel

• What is your historical track record raising assets? • What products have you marketed in the past? (more for boutiques) what level of familiarity with the fundamental and technical aspects of the asset classes that relate to those products? • What resources do you have at your disposal? • How are you compensated with respect to assets raised? • Do you currently charge any other client a lower rate for the product than you have quoted to me?

Client Service personnel

• Can you tell me your level of familiarity with the asset class in general and the product under review in particular? • Can you provide me with examples of your client communications, including research reports, commentaries, portfolio accounting/reconciliations and other communications you normally send to clients? Please indicate the timing. • How many clients do you service? • What resources do you have at your disposal? • To what extent would you be available to me if I hired your firm? • How many clients do you personally service? If there are other client service professionals at the firm, ask how many clients are distributed among the staff and ask if there is a maximum number of client relationships given to staff.

Technical/Systems Personnel

• What systems does the firm use for all elements of the investment process and portfolio management process? Who maintains the systems? • What type of internal network do you maintain? • Do you employ any kind of virtual private network to employees when they are off site? • What is your system for backing up files? • What is your disaster recovery system? • Who is your backup? • What security procedures do you employ? • Do you outsource any of the technical/systems work? • How often do you upgrade hardware and software?

Legal/Compliance Personnel

• May I have a copy of your firm’s compliance procedures? • How do you track possible employee violations of internal procedures and regulatory requirements? • Has your firm been questioned or charged with regulatory violations?

Assessing the office

• Is the firm laid out efficiently? • Does the firm have enough space to accommodate future growth? • Does the office have enough room for hard copy filing? • Does the firm keep old files on site or archive them off site? • Where are the network servers located and what if any safeguards do they employ? • What is the physical condition of the office? • What is the physical condition of the computers in the office?

Fees

Fee considerations are important in choosing investment products. Fees can be easily controlled while other factors such as performance are much harder to realize. We should always prefer products with lower fees unless it makes sense to pay more for better value-add.

Take the decision to go Active versus Passive as an example.

In assessing an Active fund, the real cost is the extra cost we would pay over the costs of an index/passive fund. The reward is the alpha or the risk adjusted excess returns of the fund.

John Palicka’s book illustrates this well with the below:

Assume that in one year, 70% of managers do not outperform the index. They all match the index. The remaining 30% of managers outperform the index by 2%. Assume we start investing with $1.00. Active funds charge 1.5% while passive funds charge 0.25% fees.

Looking at the expected value of the payoffs after fees for active management, we get 0.7 x ($1.00 – Fees of $0.015) = $0.6895 as a payoff for those who did not exceed the index. To this we add the benefits of those who did. Thus 0.3 x ($1.00 + Difference of outperformance $0.02 – Fees of $0.015) = $0.3015. Together the payoff is $0.6895 + $0.3015 = $0.991.

An index approach shows 1.00 x ($1.00 – Fees of $0.0025) = $0.9975.

Index approach gives higher expected returns.

So one would need active managers to achieve higher alpha, or have more managers outperform the index, or lower their fees.

Investment Oversight

Monitoring Of External Fund Managers

Manager Performance Review is an integral part of the investment process. In the implementation stage after the Strategic Asset Allocation is completed, external fund managers are appointed to manage various allocations. External fund managers are selected after careful due diligence is performed and objective evaluations are done. We regularly review appointed fund managers to ensure they continue to be suitable for managing our surplus funds. Managers deemed to be no longer suitable would be replaced after the manager review.

Departure or change in key personnel could greatly affect the management of the portfolio thus affecting the investment performance of the investment. The financial health of the fund management company could deteriorate, increasing our counter-party risk as we continue to engage the external fund manager. Regular monitoring of key changes such as those mentioned above allows us to take preventive measures to protect the integrity of our investments.

External fund managers are bounded by the investment guidelines given to them upon inception. We monitor the fund manager’s adherence to investment guidelines as given to them. Diverging from the investment guidelines affects the expected risk and returns characteristics of the mandate and affects the overall policy portfolio.

Description Of Key Performance Metrics

Excess Returns: Excess returns are defined as investment returns from portfolio that exceeds the given benchmark. Excess return is widely used as a measure of the value added by the portfolio manager above what would have been generated by tracking the index passively. Excess return is also known widely as the Alpha. Excess returns is the difference between a portfolio’s return and it’s benchmark’s returns.

Information Ratio: A ratio of portfolio returns above the returns of the benchmark to the volatility of those returns. The information ratio (IR) measures a portfolio manager’s ability to generate excess returns relative to the benchmark, and also attempts to identify the consistency of the investor. The higher the IR the more consistent a manager.

Sharpe Ratio: A ratio to measure risk-adjusted performance. The Sharpe ratio is calculated by subtracting the risk-free rate (such as that of the 10-year U.S. Treasury bond) from the rate of return for a portfolio and dividing the result by the standard deviation of the portfolio returns. In other words it gives the returns (excess returns above risk free returns) per unit risk.

Tracking Ratio: A divergence between the returns of a portfolio and the returns of a benchmark. Typically for a passively managed fund aiming to track the benchmark, the tracking error would be lower. On the flip side, actively managed fund aiming to outperform the benchmark would have higher tracking error.

Different investment strategies require different performance measurement ratios to accurately measure what the fund manager is supposed to achieve. Broadly speaking fund managers can be tasked to manage the portfolio “actively” or “passively”. Active fund management strategies aim to outperform the given benchmark’s risk and returns characteristics. Passive fund management strategies aim to replicate the given benchmark’s risk and returns characteristics.

As such information ratio is the most suitable measurement tool to measure active fund managers. Information ratio measures how consistent the fund manager is in outperforming the given benchmark. Tracking error is the most suitable measurement tool to measure passive fund managers. Tracking error measures how closely the fund manager tracks the given benchmark. Passive fund managers should aim to produce low tracking errors.

Other than using the most suitable measurement tool, a comprehensive review of fund manager performance requires incorporating other quantitative and qualitative assessments mentioned earlier.

Discover more from hellojayng.com

Subscribe to get the latest posts sent to your email.

No Comments